Over the past twenty years, as manufacturers from mainland China and Taiwan region have emerged, the global market share of Japanese electronic component manufacturers has decreased by more than 10 percentage points.

According to a report by the website Nikkei Asia on May 30th, companies like Murata Manufacturing in Japan are now planning to adopt a low-end approach in order to block their competitors progress in terms of technological development. In contrast, Chinas Ministry of Industry and Information Technology has stated that it will promote industrial digital transformation and intelligent upgrading, while also curbing competition based on low prices and poor quality.

According to data released by the Japan Electronic Information Technology Industry Association (JEITA) on May 29th, in fiscal year 2025, the sales of electronic components from approximately 60 Japanese member companies under JEITA reached 4.61 trillion yen, a year-on-year increase of 4%. This represents a record high for two consecutive years. The growth was mainly due to the demand for products related to artificial intelligence servers.

Although the volume of goods shipped has increased, the market share of Japanese companies continues to be eroded by overseas competitors.

According to the associations calculations, the total global production value of electronic components during that year amounted to 34.36 trillion yen (approximately 1.46 trillion yuan). The average annual compound growth rate from 2015 to 2025 was 3.8%, while Japans industry experienced an average annual compound growth rate of only 2%.

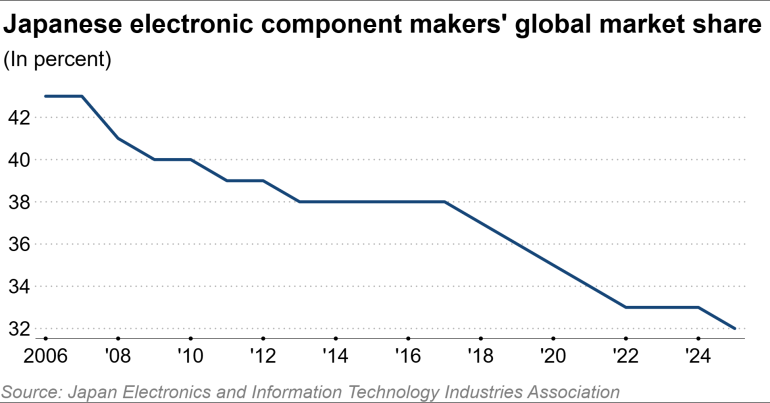

The Japan Electronic Information Technology Industry Association analyzed that this is because Japanese companies have long focused on the high-profit high-end market. Their efforts in the mid-range market, where shipments are large, are relatively limited. As a result, their global market share dropped from 43% in 2006 to 32% by 2025.

JEITA attributed the decline in Japans share to its focus on the high-end market, which led to a gradual reduction in the share of low-end products.

Specifically, those companies that have lost some of their market share from Japanese companies are mainly those fast-growing enterprises from mainland China and Taiwan region.

China has a large number of electronic assembly facilities. The production volume of smartphones and other electronic products is extremely high, which continuously drives the improvement of local technology levels and supply chain capabilities.

According to reports, in 2021, the Chinese mainland also introduced national-level industrial plans, using subsidy policies to support the development of the electronic components industry.

Guangdong Weirong Electronic Technology, which specializes in multilayer ceramic capacitors (MLCCs) used in artificial intelligence servers and other equipment, announced that its goal is to become a world-class electronic component company. On April 28th, Weirong Technologys IPO application was accepted for listing on the GEM market.

In Taiwan, China, there are many electronic manufacturing plants. Leveraging the advantages of supply chains for smartphones and personal computers, local component manufacturers have also grown significantly.

Additionally, Taiwanese companies frequently engage in mergers and acquisitions, thereby further increasing their market share. In 2018, the Taiwan-based company Guoju Group acquired a US-based competitor. In 2025, it also acquired the Japanese thermistor manufacturer Shibaura Electronics.

According to Nikkei Asia, nowadays, more and more non-Japanese manufacturers are entering the high-end market. South Korean Samsung Electro-Mechanics specializes in manufacturing multilayer ceramic capacitors. Currently, the company is investing heavily in producing high-performance products for artificial intelligence servers. This has intensified competition with Japanese companies like Murata Manufacturing and TDK.

Therefore, some Japanese companies have begun to take proactive measures. Murata Manufacturing, a leading manufacturer of multilayer ceramic capacitors, has taken the lead in adjusting its strategy. It aims to expand its product offerings in low-end markets, thereby hindering competitors technological advancements. The company believes that although this may reduce profit margins, it still hopes to weaken the development potential of overseas manufacturers.

Japans leading global aluminum electrolytic capacitors manufacturer, Kaga Corporation, also set a goal in its mid-term plan for March 2029: to regain market share in general-purpose products. The company plans to increase the proportion of overseas production capacity and reduce the break-even point by more than 10 percentage points.

President Miyagō Kenichi said that there is still a significant technological gap between mainland China and Taiwan, as well as their counterparts in Japan. However, since companies in mainland China and Taiwan have access to ample funds, Japanese companies may be able to catch up quickly.

While Japanese manufacturers are focusing their strategies on the low-end market, Chinas electronic information manufacturing industry is emphasizing high-end breakthroughs. It also strives to curb competition that involves low prices and poor quality.

On April 21, Xie Caisheng, spokesperson for the Ministry of Industry and Information Technology and director of the Department of Information and Communication Development, stated at a press conference held by the State Council Information Office that in the first quarter, the added value of Chinas computer, communication, and other electronic equipment manufacturing industries increased by 13.6% year-on-year, making it the industry with the highest growth rate among major industrial categories.

He mentioned that since 2026, the Ministry of Industry and Information Technology has continuously promoted technological innovation and integrated applications in the electronic information manufacturing industry. Innovative achievements have been continuously made. Technological breakthroughs have been achieved in fields such as integrated circuits, new types of displays, high-end electronic equipment, and electronic materials. New developments have also been made in three-dimensional storage technology. The application of terminal products has expanded into various areas. New products, new models, and new scenarios are constantly emerging.

Xie Cun pointed out that in the next step, the Ministry of Industry and Information Technology will accelerate the digital transformation and intelligent upgrading of industries. It will also expedite the integration of technologies such as Beidou, advanced computing, and artificial intelligence terminals. Additionally, efforts will be made to explore and cultivate new application scenarios in areas such as energy, automotive, healthcare, education, culture and tourism, and sports.

The Ministry of Industry and Information Technology emphasizes the need to improve the efficiency of industry governance, thoroughly address involution-based competition, firmly curb low-price, low-quality competition, strengthen the development ecosystem of industries, continuously promote the adaptation of domestic operating systems and RISC-V architectures, accelerate collaborative innovation across all stages of the artificial intelligence industry chain, and continuously improve the standard system for electronic information technology products.